THIS POST MAY CONTAIN AFFILIATE LINKS. PLEASE SEE MY DISCLOSURES FOR MORE INFORMATION

The majority of people in the workforce have a 401k plan in place. These are the most common type of retirement savings account for employees; most medium to large companies offer them to their workers.

The majority of people in the workforce have a 401k plan in place. These are the most common type of retirement savings account for employees; most medium to large companies offer them to their workers.

A 401k is one of the best ways to fund your retirement years but many people make serious mistakes when it comes to managing their plan and getting the best possible outcome.

This is because few people really understand how to make the most of their 401k. According to a survey conducted by the Employee Benefits Research Institute, the median account balance of a 401k plan is a measly $18,000. This isn’t going to take you very far in retirement!

In fact, one of the most common financial mistakes American workers make is in regard to their 401k. So I’m going to look at a few ways you can improve the management of your 401k and maximize your returns.

Table of Contents

5 Simple Steps For Taking Control Of Your 401k Plan

#1. Be In Control

The first thing to do is to be in control of your plan. Don’t just assume that your employer is doing the best for you in this regard. The worst mistake people make is ignoring their 401k and hoping it takes care of itself.

One of the benefits of a 401k plan is that you get to choose the type of securities your money is invested in. Your plan will have a range of investments to choose from, typically mutual funds, so you can create your own portfolio or group of investments.

You might think you don’t know anything about choosing investment strategies but don’t be intimidated by the process. You owe it to your financial future to take the time to select your own portfolio.

When individuals fail to choose their own portfolio, their account is often added to other ‘unloved’ plans and placed in a poor-producing, low-yielding default portfolio. That’s definitely not making the most of your money!

So make it a point to pick a portfolio. Most people can get away with 2 funds, a large cap stock fund and a bond fund. A good starting point is to put 60% of your contribution towards the stock fund and 40% towards the bond fund.

If you are open to a little more risk, which is another way of saying volatility, then you can add in small cap stock fund and an international stock fund. You should keep 25% of your contribution towards the bond fund and split up the remaining 75% between the stock funds.

At the very least, you should pick a target date fund if it is offered. Just pick the one that corresponds to when you expect to retire. This will ensure you are at least invested in the stock market and you money isn’t just sitting in cash.

#2. Take Advantage Of Free Money

The other area where you need to pay attentions to is with employer matching contributions. If your company offers matching, make sure you understand the rules and conditions that apply so that you can get the maximum matching contribution.

This is effectively free money, to which you are entitled, so take full advantage of it.

Here is how it works. Say your employer offers you a 50% match on the first 5% you put into the plan and you earn $50,000 a year.

At the end of the year, you will have contributed $2,500 into your account. Your employer will have given you $1,250 just for contributing to your 401k plan! It baffles me why so many people turn down free money.

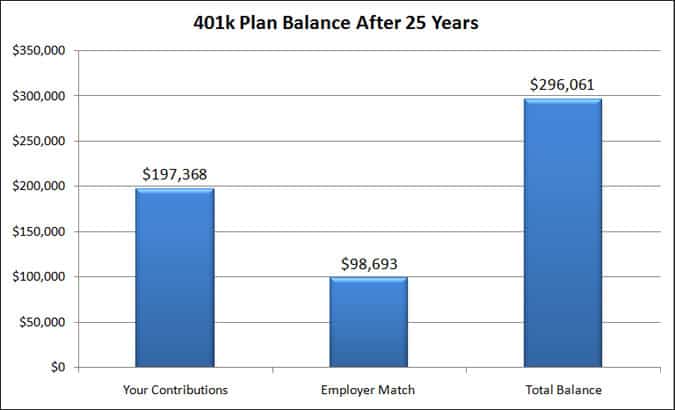

Assuming an annual 8% return and working 25 years, your 401k plan balance will be close to $100,000 higher just from your employer contributions and the gains on that money. That has a serious impact on your retirement savings!

The only catch to matching contributions is that most employers require you stay with the company for 5 years. Once you clear this threshold, any money they contribute to your 401k plan is yours to keep.

#3. Contribute The Maximum

You also need to make sure you are making the maximum allowable contribution to your 401k plan. In a recent survey, it was found that on average, American workers were contributing less than 7% of their salary, which is well below the allowable amount.

If necessary, look at your personal budget for ways to shave some areas of spending, to free up the money to maximize your plan.

If contributing the maximum amount right now is too much of a stretch for you, try to save 10% of your salary. Then every year, add another 1%. Following this format will slowly increase your contributions so that you never realize you are saving a little more each year.

The money you put into your 401k is tax-deferred which means that you don’t pay tax on it until you withdraw funds after you retire. Because of the positive effect of compounding interest, you will be ahead, so get as much money paid into your account as possible.

If you are over 50, make sure you take advantage of the increased contributions you are allowed to make. These catch-up payments are especially helpful to workers who have left saving for retirement until later in life.

#4. Watch Out For Fees

Cutting the costs associated with your 401k plan is another good management strategy. Many companies invest their employees’ 401k funds in mutual funds that come with high fees, which essentially eat away at your return on investment. Even an extra 1% in fees can negate nearly all the tax benefits your plan provides.

Unfortunately, many of the fees associated with a 401k plan have been hidden. In other words, you would have a tough time trying to figure out just how much money you were paying in fees.

Luckily though, you can use Personal Capital. It’s a free service that lets you link your 401k plan. They crunch some numbers and tell you exactly how much you are paying in fees each year.

They even will show you over time what this amount adds up to. Be sure you are sitting down for this! You can get started with Personal Capital here.

Once you have this information at hand, you can pick some lower cost investments in your 401k plan and save yourself a lot of money.

#5. Keep Saving

The last big mistake people make in relation to their 401k occurs when they leave their job. At that time, you usually have the option of how you receive your balance. You can choose to take it all as a lump sum, to get periodic payments or to roll the whole balance over into another 401k or an IRA. Sometimes the employer offers the option of leaving the balance where it is.

The best option is to roll it over into another employer’s plan or IRA. Your money is not taxed in these circumstances and your retirement plan stays intact. By rolling over your 401k plan, you keep control of the investments and keep your savings growing tax deferred.

If you choose to take the money, it will be subject to tax so you will lose 20%. You would also have to start saving for retirement all over again, which will put you behind the eight ball to say the least!

Continue what you started and roll your retirement fund over into another retirement fund so you don’t lose ground in the financial stakes. You can get detailed information on rolling over your retirement plans in this post.

Final Thots

Look after your 401k effectively and efficiently and let your employer and the government to help fund your retirement. The employer-matched contribution is free money. The tax-deferred element gives you an up front tax benefit.

Know the rules so that you can maximize these benefits and have more money in your retirement years.

So readers, how are you making the most of your 401K?

How interesting that you found that the median account balance of a 401k plan is a measly $18,000 — that’s the max amount that you’re allowed to contribute in one year!

For me, I’m not maxing mine out yet because I’m really focusing on paying off debt right now

Definitely love the idea of free money so getting the employer match is crucial. Over the past few years, I’ve slowly worked my way up from just enough to get the employer match to what I believe to be the recommended amount, 15% of my income. It took a while but it feels good to be here! I agree with the fees point, fees are a sneaky thief that will lower your return. I compare funds available to me both by average return and the type of fund (i.e. growth or target date) but also by the expenses. I was shocked how much some funds were charing compared to others! Although not mentioned in the article, I do save consistently. I know some folks will adjust their contributions based on the market, but me personally, I just put away 15% each paycheck. I don’t think timing the market is feasible and just keep saving!