THIS POST MAY CONTAIN AFFILIATE LINKS. PLEASE SEE MY DISCLOSURES FOR MORE INFORMATION

There is a strong movement by many people to become debt free. I personally think this is a great choice. Learning to live within one’s means is one of the keys to financial success.

There is a strong movement by many people to become debt free. I personally think this is a great choice. Learning to live within one’s means is one of the keys to financial success.

Too many people spend everything they earn each month and in some cases spend more. By not saving anything, they have zero shot at improving their financial situations. They are stuck financially in life, never getting ahead.

For those of you that are still living beyond your means, I suggest you make an effort to get out of debt. I say this for one simple reason. Debt is bad.

Why is debt bad you might ask? In this post, I am going to show you how debt limits you in life in more ways than you might think.

Table of Contents

Simple Reasons Why Debt Is Bad

#1. Debt Ties You Up In Bad Times

The first reason why debt is bad is because debt is a burden. But you won’t feel the true consequences of debt until times get tough. I think so many people are getting out of debt now because they had this wake-up call during the recession. Here is what I am talking about.

Let’s say you have $10,000 in debt that you are taking your time paying off. I won’t get into the whole argument of how much interest you’ll be paying, but rather I want to simply focus on your monthly payment. Let’s say that the monthly payment for that $10,000 of debt you have is $200.

While this $200 seems inconsequential now, what happens if you lose your job or become disabled and cannot work for a few months? You might be thinking that the $200 is still small, but over time, it adds up.

If you are unemployed, that $200 is money you could be using to buy groceries for your family. Or, it could simply mean $200 extra dollars a month which will help to cover your basic living expenses for a few months until you find a job.

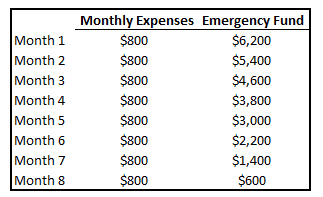

Look at the chart below. It assumes that you have $7,000 in an emergency fund and that after cutting out all non-essentials, your monthly expenses are $800. This includes $200 for debt repayment. After 8 short months, you have run your emergency fund dry.

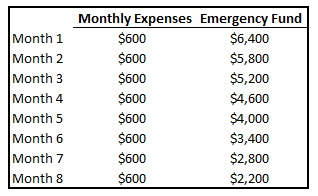

Now look at the same chart, but you don’t have your monthly debt payment. After 8 months, you are still in decent shape.

So while you have a job and an income, make it a point to get rid of your debts quickly. This might mean you have to shift things around in your budget. If so, do it. Don’t run the risk of having to scrape by if you do lose your job.

Finally, resist the urge to convince yourself that your job is safe. Not job is permanent. In addition to this, you could easily get hurt doing something simple and end up needing to take an extended time off work.

#2. Debt Adds Stress To Life

The second reason why debt is bad is because money causes a lot of stress in our lives. When we are unemployed, our stress levels rise as we worry about how we are going to make ends meet. Why not limit that stress by making sure our finances are in good shape should the unfortunate occur?

Having debt just adds more fuel to a stressful situation. Suddenly you are short tempered with loved ones and say or do things you regret.

It’s not worth it. Avoid this completely by making sure you have zero debt.

Solutions To Running Out Of Money

You have two options when it comes to solving the crisis I pointed out above.

- Have a much larger emergency fund

- Get rid of the debt

Having a large emergency fund is important to financial success. At the very least, you should have $1,000 saved in an emergency fund at all times. Once you have $1,000 then you should focus on getting rid of your debt.

Doing so will make the bad times more tolerable because you won’t be as worried with running out of money. The stress will still be there, but not like it will be if you have debt repayments to make.

Once you have your debts paid off, then you can begin to work on increasing the amount in your emergency fund. Try to get it so the amount equals 9 months worth of living expenses. In other words, if you total up your monthly expenses and they come to $2,000 then you need to have $18,000 in an emergency fund.

To some, this amount might seem high. You have two options. First, save the $18,00a and keep living life as you currently are. Or, you can do the math to figure out what your monthly expenses would be if you just kept the basics. Assume you have no income coming in. What things can you live without for a period of time?

Strike them out of the budget and take this new lower number and multiply it by 9. Let’s say your lower number is $1,000. Now you only need to have $9,000 in your emergency fund.

Final Thots

The bottom line is that debt is bad.

I encourage you to do a quick analysis of your situation. Total up how much you spend each month and take out all unnecessary items. Then look at how large your emergency fund is and divide the two. How many months will your emergency fund last? Whatever answer you end up with is how many money you can survive financially without an income.

Run the numbers again without the debt repayment and see what it looks like now. If you are still in bad shape, I encourage you to start paying off your debt.

Your goal in either case is to have that number be 9 or more. This means you can survive at least 9 months without an income. While you might think 9 months is a long time to go without an income, remember that landing a job isn’t a simple process any longer.

And you may find the job offers you are getting pay a lower salary than you were earning before. Having extra cash in an emergency fund will help you survive on a smaller income.

Just remember that you won’t get out of debt overnight. But the more you debt you can pay off, the more thankful you will be should the unfortunate happen.

I agree that most debt is an albatross, and that it’s important to get out of debt to free up your cash flow and allow you more options and more long term portfolio growth potential. I also believe that taking on certain debts (like a mortgage) can help you leverage more options. Not all risk is “bad risk” if you take the appropriate measures to mitigate, and certain debts can help you get further ahead.

In the event of job loss, don’t forget the power of flexibility. If you can cut things down to the bare bones, your emergency fund can last much longer. Just because you spend $800/month now, it doesn’t mean you need to spend it if you’ve lost your job. (Unless you’re already living a bare-bones life…)